Inflation, interest rates and household spending are closely interconnected forces that shape the broader direction of an economy. When prices rise, purchasing power shifts; when borrowing costs change, consumer behaviour often follows. Central banks monitor this relationship carefully, as household consumption typically represents a substantial portion of national economic output. Understanding how these elements interact provides valuable insight into both short-term economic trends and longer-term structural adjustments. Economists and market commentators such as Kavan Choksi frequently emphasise that consumer confidence and credit conditions are central to maintaining economic momentum.

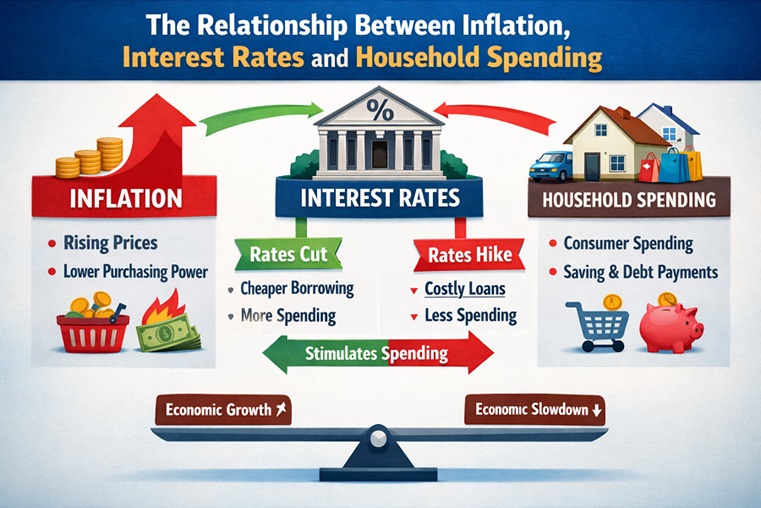

Inflation directly affects household budgets by increasing the cost of goods and services. Essentials such as food, energy and housing often feel the impact most immediately. When prices rise faster than wages, real income declines, forcing households to adjust spending habits. Discretionary purchases may be postponed, savings rates can fall and reliance on credit may increase. Over time, persistent inflation can alter consumption patterns, shifting demand toward lower-cost alternatives or reducing overall expenditure.

Interest rates serve as a key policy tool to manage inflation. When central banks raise rates to combat rising prices, borrowing becomes more expensive. Mortgage payments may increase, personal loan costs rise and credit card interest rates climb. Higher financing costs typically dampen household spending, particularly on large purchases such as homes, vehicles and durable goods. While this cooling effect can help stabilise prices, it also slows economic growth if consumption contracts significantly.

Conversely, when inflation subsides and central banks lower interest rates, borrowing becomes more affordable. Households may feel more confident taking on new loans or refinancing existing debt at lower rates. Reduced debt servicing costs can free up disposable income, encouraging greater spending. This dynamic often supports economic recovery following periods of slowdown.

Expectations play a crucial role in this relationship. If households believe inflation will remain high, they may accelerate purchases to avoid paying higher prices later. This behaviour can further stimulate demand and complicate efforts to stabilise prices. On the other hand, if confidence in monetary policy remains strong and inflation expectations are well anchored, consumers are less likely to alter spending dramatically.

Employment conditions also influence how inflation and interest rate changes affect households. Strong labour markets and steady wage growth can offset some of the pressure caused by rising prices or higher borrowing costs. In contrast, weak employment prospects may amplify the negative impact on consumption, deepening economic slowdowns.

Ultimately, the interaction between inflation, interest rates and household spending forms a feedback loop within the economy. Policymakers must balance price stability with growth objectives, recognising that overly aggressive tightening can suppress demand, while insufficient action may allow inflation to persist. For households, adapting to changing economic conditions requires careful financial planning and awareness of how shifts in policy influence both costs and opportunities.